Objective of TDS Section 194IA

While introducing TDS on immovable property the Finance Minister said that transactions of immovable property were usually undervalued and under-reported. Almost half of the transactions did not even carry the PAN number of the parties concerned. Th us, in order to prevent undervaluation and under-reporting of transactions in the real estate sector and to systematize tax provisions and ensure early collection of tax Section 191A has been introduced vide Finance Act, 2013. Th is section is eff ective from 1st June 2013. Special Article – TDS on sale of Immovable Property – TDS Section 194IA

Concept of TDS u/s 194-IA

TDS is required to be deducted at source as per provisions of section 194-IA of the Income-tax Act, 1961 (‘the Act’). Th e provisions of section 194-IA are as under: “(1) Any person, being a transferee, responsible for paying (other than the person referred to in section 194LA) to a resident transferor any sum by way of consideration for transfer of any immovable property (other than agricultural land), shall, at the time of credit of such sum to the account of the transferor or at the time of payment of such sum in cash or by issue of a cheque or draft or by any other mode, whichever is earlier, deduct an amount equal to one per cent of such sum as income-tax thereon. (2) No deduction under sub-section (i) shall be made where the consideration for the transfer of an immovable property is less than fi fty lakh rupees (3) Th e provisions of section 203A shall not apply to a person required to deduct tax in accordance with the provisions of this section.”

The provision can be summarised as under:

Definitions

“Immovable Property” means any land (other than agricultural land) or any building or part of a building. Example; Shop, Godown, theater etc.“Agriculture land” means agricultural land in India, not being land situated in any area referred to in items (a) and (b) of sub-clause (iii) of clause (14) of section 2 i.e. It is situated within the jurisdiction of municipality which has population of not less than 10000; or It is situated in any area mentioned below:

Take Aways: On analysis of above definition of agricultural land it can be said that

Urban agricultural land is not considered as agricultural land and thus is covered under provisions of section 194 IAImmovable property could be located in India or outside India.

Analysis of Section 194IA:

Provisions of section 194-IA are triggered when transaction has been entered after01.06.2013 and payment consideration is Rs. 50,00,000 or aboveSection 194IA is applicable in case of gift from relatives also. However, if transfer is made without payment of any consideration, then provisions of this section will not applyProvisions of Section 194–A does not apply for consideration received under the compulsory acquisition of the property as mentioned in section 194-AIn case the seller is the non-resident provisions of section 194-IA will not apply. Th e same is covered by section 195 of the Act.

Rate of TDS

The registration for transfer of immovable properties cannot be done unless the transferee provides proof of deduction of tax at source and payment thereof to the registering officer. Procedural Requirement :

Procedure for Payment of TDS: Tax deductor (Buyer) has to furnish information regarding the transaction online in Form 26QB; after furnishing of details of the transaction deductor (i.e. Buyer) is required to make online payment of tax withheld. Time for depositing of TDS TDS is required to be deposited within a period of 7 days from the end of the month in which deduction is made. Issuance of TDS Certificate to Seller : Buyer is required to issue a TDS Certifi cate in Form No.16B within 15 days from the due date of furnishing the challan cum statement in Form No. 26QB; Seller can verify deposit of taxes deducted by the buyer in his Form 26AS [Annual Tax Statement].

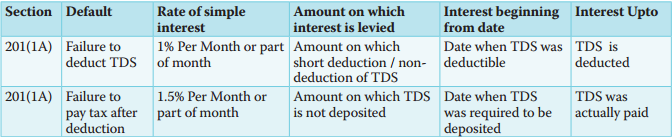

Penal Provisions For Non – Compliance:

(A) Interest: (B) Penalty: As per section 271C of the Act, penalty for non deduction / non-payment of TDS is equal to the amount of tax which the assessee failed to deduct or pay [Th is penalty shall be imposed by the Joint Commissioner].