2. Status Of Corporate Debt Restructuring (Cdr) And Non Performing Assets (NPAS)

3. Eligibility

Conversion of outstanding debts can be done by a consortium of lending institutions. Such a consortium is known as the Joint Lenders Forum (“JLF“).The JLF may include banks and other financial institutions such as NBFCs.The Scheme will not be applicable to a single lender.

4. Conditions

At the time of initial restructuring, the JLF must incorporate an option in the loan agreement to convert the entire or part of the loan including the unpaid interest into equity shares if the company fails to achieve the milestones and critical conditions stipulated in the restructuring package.

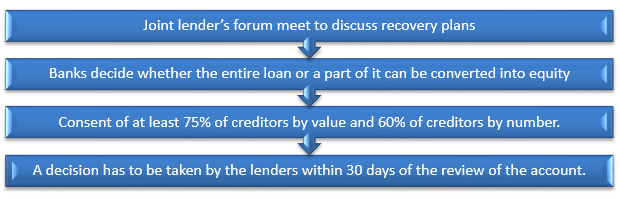

This option must be corroborated with a special resolution since the debt-equity swap will result in dilution of existing shareholders.Such a mandate will result in the lenders acquiring a majority (51%) ownership.“If the company fails to achieve the milestones stipulated in the restructuring package, the decision of invoking the SDR must be taken by the JLF within thirty (30) days of the review of the account during the restructuring.The JLF must approve the debt to equity conversion under the Scheme within ninety (90) days of deciding to invoke the SDR.The JLF will get a further ninety (90) days to actually convert the loan into shares.

5. What happens after the debt-equity swap?

On completion of conversion of debt to equity as approved under the Scheme, the JLF shall hold the existing asset status of the loan for another eighteen (18) months.The JLF must divest their holdings in the equity of the Company. If the JLF decide to divest their stake to another Promoter, the loan will be upgraded to ‘Standard’. The ‘new promoter’ should not be a person/entity from the existing promoter/promoter group.

6. Need For Strategic Debt Restructuring

According to Fitch, stressed assets of Indian lenders set to rise 13% of total advances by March, 2016 from 10.73% as at December, 2014CRISIL ratings & S&P’ Indian arm estimates the total bad loans to reach Rs.5.3 trillion by March, 2016Failure of Debt Restructuring package.

7. Process of SDR

8. Valuation For Conversion Of Debt Into Equity

The conversion price of the equity shall be determined as follows:

9. Open offer? Or not?

The pricing formula stated above has been exempted from the Securities and Exchange Board of India (SEBI) (Issue of Capital and Disclosure Requirements) Regulations, 2009.Further, the acquiring lender on account of conversion of debt into equity will be exempted from making an open offer under Regulation 3 and Regulation 4 of the provisions of the Securities and Exchange Board of India (Substantial Acquisition of Shares and Takeovers) Regulations, 2011.

10. Difference Between Corporate Debt Restructuring(CDR) And Strategic Debt Restructuring(SDR)

11. Advantages to Banks

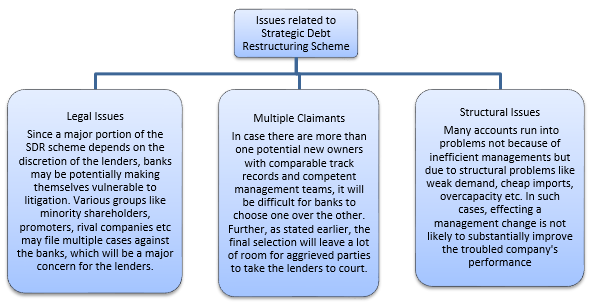

12. Issues Related To Strategic Debt Restructuring Scheme

13. Analysis

RBI has recently proposed this concept in India. Although banks would get ownership and control over these corporates, at this stage, the value of the underlying assets would have deteriorated substantially. Banks are, in effect, left with a bagful of non-performing assets. It will be challenging for the lenders to continue to run the business of these companies till the time a suitable buyer is found and may have to deploy professional management to efficiently run and manage these companies leading to “putting good (public) money behind bad money”. Until these corporates turn-around and become viable, finding a suitable buyer for the lenders will be difficult and may take many years. SDR can be considered as a last resort to revive such companies which have already undergone a long drawn financial restructuring process.One of the critical problems of the Scheme could be the price at which the debt to equity conversion must take place. The conversion price could be higher than the market price as the market value of these scrips would have substantially reduced, whereas the lenders as per the Scheme will be required to convert the debt into equity at a price which shall not exceed the fair value (i.e. market value or break-up value, whichever is lower subject to the floor of face value). This may result in further losses to the lenders.

Sumat Singhal (B.Com, CAIIB, DTIRM, ACA, ACS, CWA(F)