At the consumer level, GST would reduce the overall tax burden, which is currently estimated at 25-30%. Any major macro-economic reforms in the country are only possible with effective fiscal & monetary policies in place and economic reforms are important for empowerment of poor. Approximately 70% of the population lives in rural India, GST will become a catalyst for a common rural market in our country with the removal of state level barriers. However, one change which every taxpayer is going to face immediately will be in their tax identification number.

Know your GSTIN, What is GSTIN?

GST Number (GSTIN) is a unique 15 digit number which is allotted to the assessee at the time of filing an application for registration for Goods & Service Tax. Just like PAN Card No is required for payment and filing of Income Tax Returns, similarly GSTIN is required for payment and filing of GST Returns.

Tracking of GST Status

Click Here to Track GST Registration Status (Detailed Procedure)

How to Track GST Status

Click here to Check GST ARN StatusClick Here to Check GST Provisional ID StatusSearch Tax Payer by GSTIN Number, UIN Number or Search GST Number

The registration in GST is PAN based and State-specific. The supplier has to register in each of such State or Union territory from where he affects supply. In GST registration, the supplier is allotted a 15-digit GST identification number called “GSTIN” and a certificate of registration incorporating therein this GSTIN is made available to the applicant on the GSTN common portal. The first 2 digits of the GSTIN is the State code, next 10 digits are the PAN of the legal entity, the next two digits are for entity code, and the last digit is the checksum number. Registration under GST is not tax specific which means that there is single registration for all the taxes i.e. CGST, SGST/UTGST, IGST and cesses. A given PAN based legal entity would have one GSTIN per State, that means a business entity having its branches in multiple States will have to take separate State wise registration for the branches in different States. But within a State an entity with different branches would have single registration wherein it can declare one place as principal place of business and other branches as additional place of business. However, a business entity having separate business verticals (as defined in section 2 (18) of the CGST Act, 2017) in a state may obtain separate registration for each of its business verticals. Further a unit in SEZ or a SEZ developer needs to necessarily obtain separate registration.

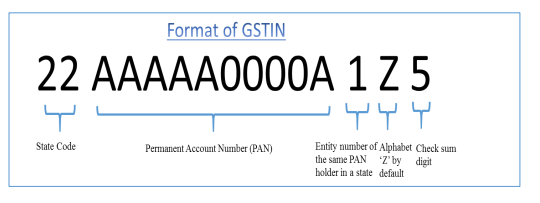

Format of GSTIN

Goods & Service Tax Identification Number (GSTIN) is a PAN based number i.e. to say that it is based on the PAN No. of the applicant. It is a 15 digit number and format of the same is as follows:-

The first two digits of this GST number will represent the state codeThe next ten digits will be the PAN number of the taxpayerThe thirteenth digit will be assigned based on the number of registration within a stateThe fourteenth digit will be Z by defaultThe last digit will be for check code

Registration under GST is not tax specific, which means that there is single registration for all the taxes i.e. CGST, SGST/UTGST, IGST and cesses. A given PAN based legal entity would have one GSTIN per State, that means a business entity having its branches in multiple States will have to take separate State wise registration for the branches in different States. But within a State, an entity with different branches would have single registration wherein it can declare one place as principal place of business and other branches as additional place of business. However, a business entity having separate business verticals (as defined in section 2 (18) of the CGST Act, 2017) in a state may obtain separate registration for each of its business verticals.

Issue of registration certificate

An application has to be submitted online through the common portal (GSTN) within thirty days from the date when liability to register arise. The Casual and Non-Resident taxable persons need to apply at least five days prior to the commencement of the business. For transferee of a business as going concern, the liability to register arises on the date of transfer. Subject to the provisions of section 25(12), where the application for grant of registration has been approved under rule 2, a certificate of registration in form GST REG-06 showing the principal place of business and additional place(s) of business shall be made available to the applicant on the Common Portal and a Goods and Services Tax Identification Number (hereinafter in these rules referred to as “GSTIN”) shall be assigned in the following format –

(a) two characters for the State code(b) ten characters for the PAN or the Tax Deduction and Collection Account Number(c) two characters for the entity code; and(d) one check sum character – Rule 3(1) of Registration Rules.

Display of registration certificate and GSTIN on the name board

Every registered person shall display his certificate of registration in a prominent location at his principal place of business and at every additional place or places of business. Every registered person shall display his GSTIN on the name board exhibited at the entry of his principal place of business and at every additional place or places of business – Rule 10 of GST Registration Rules. Recommended Articles

GST RefundGST ReturnGST FormsGST RateGST RegistrationWhat is GST?GST Invoice FormatITC under GSTHSN CodeGST LoginGST RulesGST StatusTrack GST ARNTime of Supply

If you have ay query or suggestion regarding “Know your GST Number, Know your GSTIN” then please tell us via below comment box…